"I prefer a boring company to an exciting one. Exciting companies tend to be overrated and often fail to meet expectations."

John Neff.

ELECTROMED

Ticker: ELMD

This company has been popping up in my rankings for years. It's always there, with its little red vest and its steady upward trend. It has a market capitalization of 257 million. It has outperformed the S&P 500 over several periods.

Last year, it did so spectacularly, at 187% versus 24%.

They only sell one product. Boring. Basic. Retro.Very niche. If you see it on the ground, you'd leave it there or kick it away.

This is an expectoration vest. Yes, a vest for expelling mucus. Can one expel mucus with a vest? Apparently so.

The vest inflates with air in spasms, these spasms affect the thoracic cavity and help people with respiratory problems to expectorate.

It's not a SpaceX rocket, but if you're drowning in your own mucus, you'll pay more for this vest than for a ticket to Mars.

FUNDAMENTALS

And now come the fundamentals. They are good, very good.

Growing sales, EPS with an upward trend.

Very good returns on capital. No dilutions. No debt. No dividend. Good operating margin.

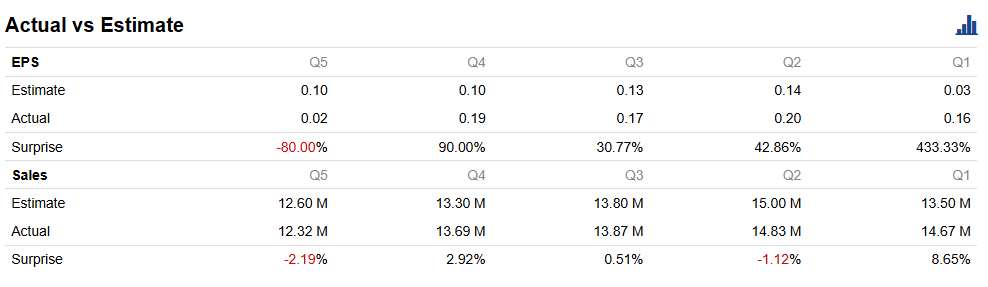

The surprise in the results forecasted by analysts has been tremendous this year, especially in EPS.

Awesome Net Income, with a CAGR of 29%.

TECHNICAL

Technically, it's working perfectly. Although a correction is likely imminent, and it may have already started.

Waiting for the price to reach the $27 range could be a good option, if you expect the price to continue rising

CYCLES

Based on the cycles, we can expect a dip soon, followed by a rise until April.

FINAL THOUGHTS

ELMD's management stands out for its conservative approach, as evidenced by its lack of debt, a key factor contributing to its financial stability.

Its high level of specialization and single-product model are both its greatest strength and its biggest vulnerability.

This specialization allows it to excel against competitors in the sector.

However, any disruptive innovation in the field of bronchiectasis, such as a pill capable of curing it, could render the SmartVest obsolete and undermine its business model.

As for its valuation, although its P/E ratio of 42 may seem high, the company's rapid growth and small size could justify the growth expectations reflected in its current price. This suggests an attractive potential for investors who trust in its ability to expand.

And that's it for today's article. If you enjoyed it, be generous and share it with others.

Thanks for reading!!!